The eIOU Wallet enables seamless value transfer through a network of

trusted connections. Each user can create their own digital tokens (like

"Alice-USD") that represent their creditworthiness. When you connect with

someone, you decide how much of their tokens you're willing to hold,

creating a web of trust that enables instant transfers.

Direct Transfer

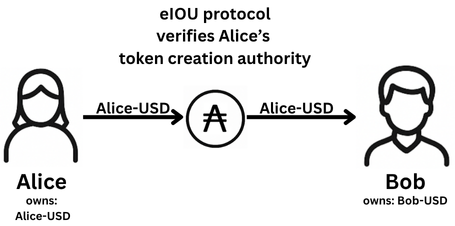

Alice wants to send Bob $100 in Alice-USD tokens

Alice creates and sends her own Alice-USD tokens to Bob.

- Alice initiates a transfer of $100 Alice-USD tokens to Bob

- The eIOU Protocol verifies Alice's token creation authority

- Bob receives $100 worth of Alice-USD tokens instantly

- Transaction is saved by both users privately

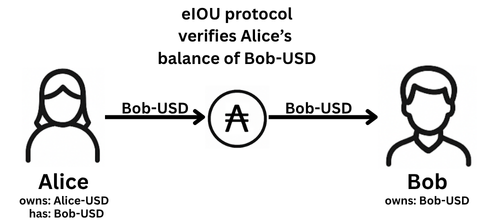

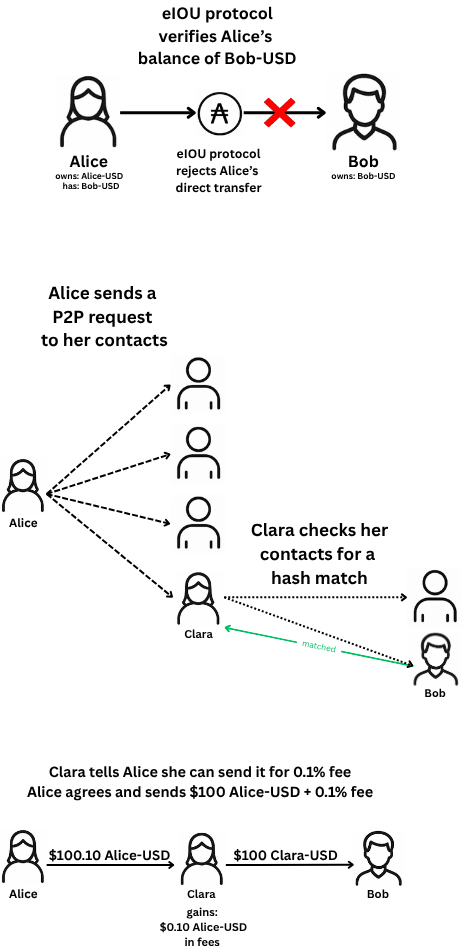

Alice wants to send Bob $100 in Bob-USD tokens

Alice has $100 worth of Bob-USD tokens in her available credit.

- Alice initiates a transfer of $100 Bob-USD tokens to Bob

- The eIOU Protocol verifies Alice's balance

- Bob receives $100 worth of his tokens instantly

- Transaction is saved by both users privately

Multi-hop Transfer

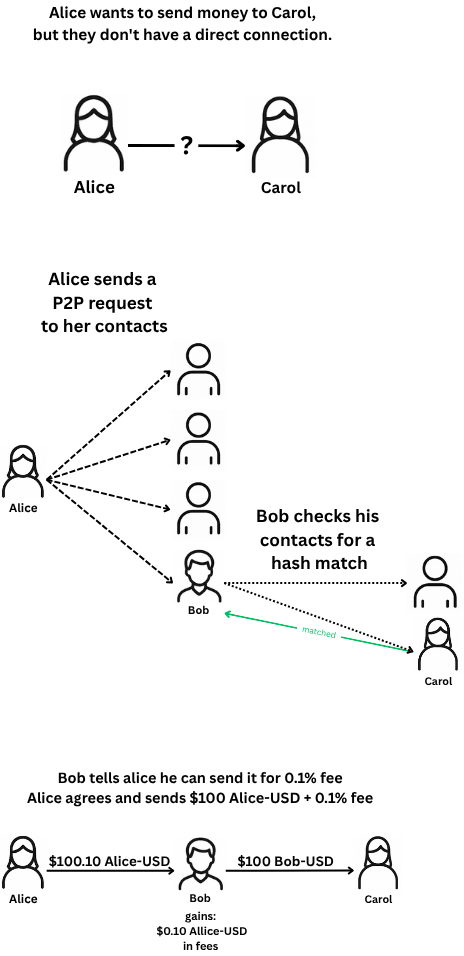

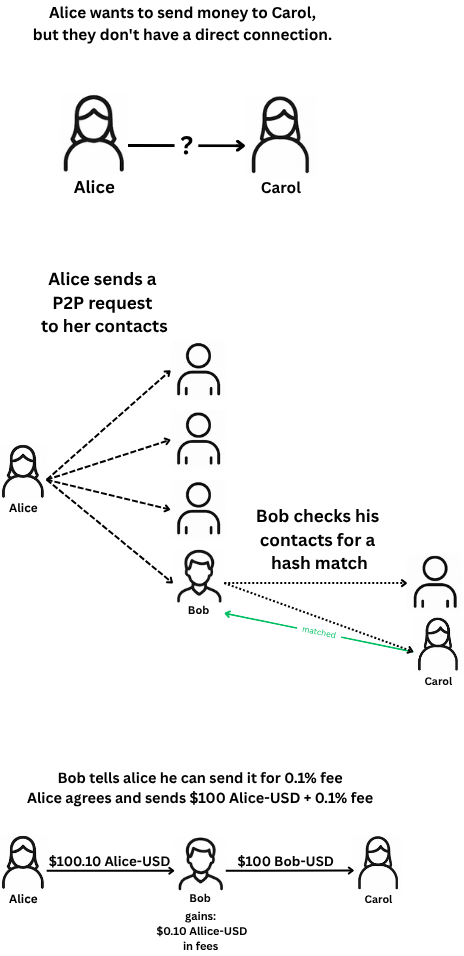

Alice wants to send Carol $100 via Bob using their respective tokens

Alice wants to send money to Carol, but they don't have a direct

connection. Bob, who has credit with both Alice and Carol, acts as an

intermediary. Bob can charge a small fee for taking on the risk of

routing the transfer.

-

Alice sends a Peer to Peer request searching for someone who can

send $100 USD to Carol

-

Bob calculates the hash for each of his contacts, checking if any

match the hash Alice sent

-

Bob finds a match, and informs Alice he can send it for a 0.1% fee

- Alice initiates a transfer of $100.10 Alice-USD tokens to Bob

- Bob receives $100.10 worth of Alice-USD tokens

- (If Alice has $100.10 Bob-USD she could use that too)

- Bob then sends $100 Bob-USD tokens to Carol

- Carol receives $100 worth of Bob-USD tokens

- All transactions are saved privately by each participant

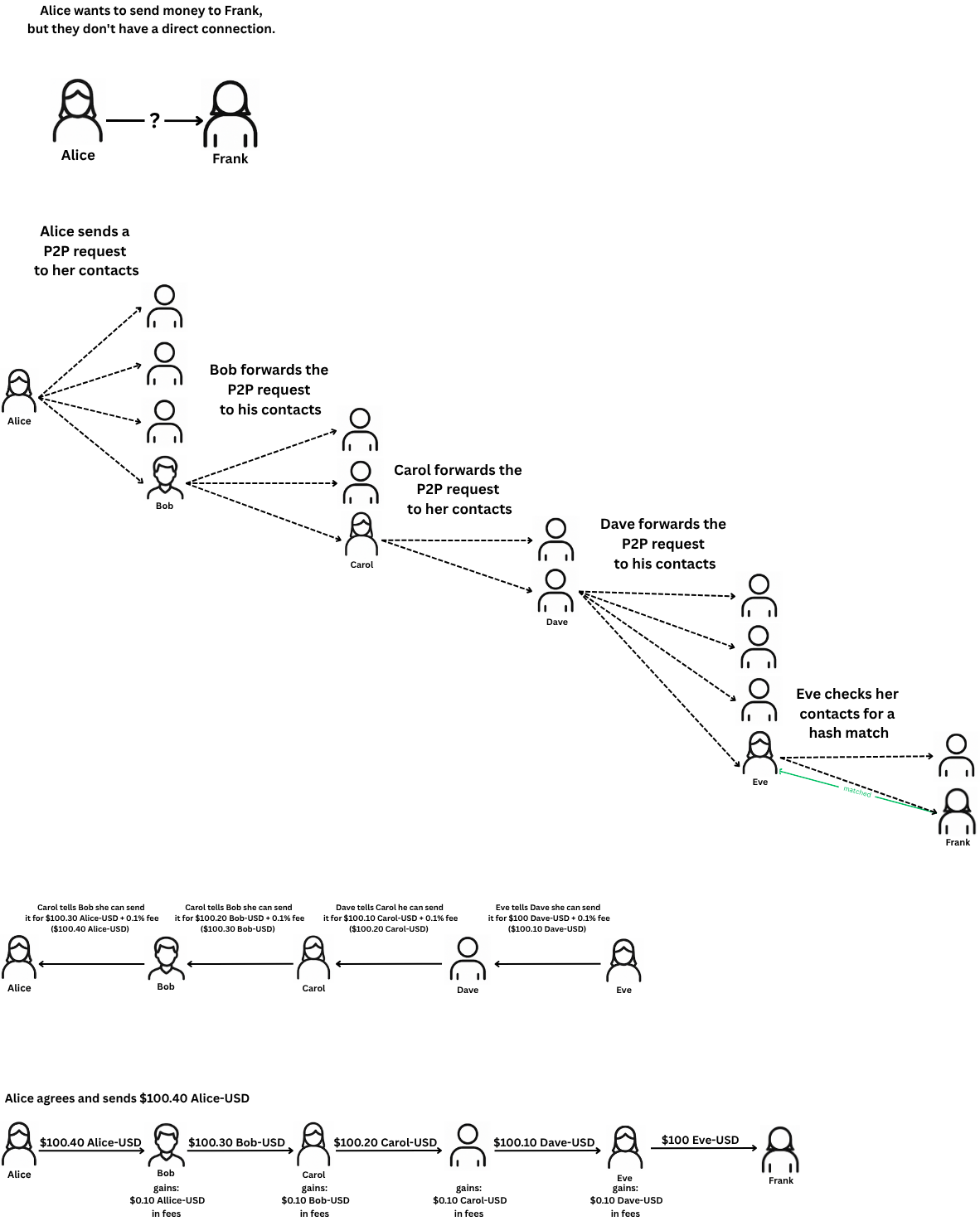

Complex Network Transfer

Alice wants to send money to Frank through multiple intermediaries

(Bob, Carol, Dave, Eve). Each intermediary can charge a small fee for

routing the transfer and taking on risk.

-

Alice wants to send $100 USD to Frank, but he is not a contact of

hers

-

Alice sends a Peer to Peer request searching for someone who can

send $100 USD to Frank

-

Alice hashes the her request (e.g. send $100 USD to Frank), along

with the time, and a salt

-

Bob calculates the hash for each of his contacts, checking if any

match the hash Alice sent

- Bob does not find a match, and forwards it to his contacts

- Carol does not find a match, and forwards it to her contacts

-

Dave does not find a match either, and forwards it to his contacts

-

Eve finds a match, checks her credit with Frank, and informs Dave he

can send it for a 0.1% fee, $100.10 Dave-USD

-

Each peer adds their desired fee, for simplicy we'll say it's 0.1%

for all of them. Dave asks for $100.20 Carol-USD, Carol asks for

$100.30 Bob-USD, and Bob asks for $100.40 Bob-USD

-

Through collaboration, Alice's peers find a route: Alice → Bob →

Carol → Dave → Eve → Frank

-

Alice accepts the fee, and sends it on to Bob, Bob to Carol, etc

-

Each node in the path automatically forwards the payment, taking on

the risk with the previous sender

- Frank receives the $100 Eve-USD

-

Debts are created along the chain: Alice owes Bob, Bob owes Carol,

etc.

Trust-based Transfer

Alice wants to send Bob $100 in Bob-USD tokens but needs credit

Alice wants to send money to Bob but doesn't have sufficient Bob-USD

tokens. Her friend Carla provides trust by accepting Alice-USD tokens.

- Alice requests a transfer of $100 Bob-USD tokens to Bob

- Bob rejects Alice's transfer request

-

Alice sends a Peer to Peer request searching for someone who can

send $100 USD to Bob

-

Carla calculates the hash for each of her contacts, checking if any

match the hash Alice sent

-

Carla finds a match, checks her credit with Bob, and informs Alice

he can send it for a 0.1% fee

- Carla's trust is used to guarantee the payment

- Carla receives $100.10 worth of Alice-USD tokens

- Bob receives $100 worth of Carla-USD tokens

Business Use Cases

Supplier Payment Chain

A manufacturer needs to pay multiple suppliers in a chain. Each

supplier can create their own tokens (e.g., SupplierA-USD,

SupplierB-USD).

- Manufacturer initiates payment to final supplier

- eIOU Protocol automatically splits and routes payments

-

Each supplier receives their portion in tokens they are willing to

accept, either that of their trusted partners or their own tokens

- All transactions are settled simultaneously

-

Suppliers can settle with each other, the manufacturer, or customers

through traditional means (bank transfers, trade credit, etc.)

Retail & Online Payments

Point of Sale Integration

A café owner wants to accept eIOU Wallet payments alongside

traditional payment methods. The café creates Café-USD tokens that

customers can hold.

- Payment terminal is integrated with eIOU Wallet

- Customer scans QR code or taps their phone

- Payment is processed instantly through the network

-

Merchant receives funds in tokens they are willing to accept,

including Café-USD tokens

-

Merchant can sell Café-USD tokens, same as they would use gift

cards, and settle with customers through various means (cash, bank

transfer, or keep the credit for future purchases)

Online Store Checkout

An e-commerce platform integrates eIOU Wallet for seamless online

payments. The store creates Store-USD tokens that customers can hold.

-

Customer selects eIOU Protocol at checkout, and pays using eIOU

Wallet

- Payment is routed through the network

- Order is confirmed instantly

-

Merchant receives payment in tokens they accept, including Store-USD

tokens

-

Merchant can sell Store-USD tokens, the same as they would gift

cards, and settle with customers through various means (bank

transfer, store credit, etc.)

Restaurant Payment System

A restaurant chain implements eIOU Wallet for table payments and staff

tips. The restaurant creates Restaurant-USD tokens, and staff can

create their own Staff-USD tokens.

- Customers can split bills automatically

-

Tips are distributed instantly to staff in tokens they accept,

including Staff-USD tokens

-

Payments are settled in real-time in tokens they accept, including

Restaurant-USD tokens

- No need for cash handling or card processing fees

-

Staff can settle with the restaurant through various means (bank

transfer, cash, etc.)

Supermarket Checkout

A supermarket chain adopts eIOU Protocol for faster checkout

experiences. The supermarket creates Market-USD tokens that customers

can hold.

- Self-checkout terminals accept eIOU Wallet payments

- Customers can pay with their phones

- Loyalty points are automatically credited

- Receipts are stored digitally

-

Customers can settle with the supermarket through various means

(bank transfer, store credit, etc.)

Settlement Options

Flexible Settlement Methods

When it's time to settle debts in the eIOU network, users have

multiple options to transfer value back through the network.

-

Bank transfers can be used to settle debts with any connected user

-

Cash payments can be made in person and recorded in the network

- Goods and services can be exchanged to settle debts

- Work or labor can be provided to settle outstanding balances

-

Users can choose how to maintain the credit relationship for future

transactions

Business Settlement Example

A supplier and manufacturer can settle their eIOU tokens through

various business arrangements.

- Traditional bank transfers or wire payments

- Trade credit for future orders

- Exchange of goods or services

- Extended payment terms with interest

- Combination of multiple settlement methods

Real-world Credit Example

Let's use a simple example of lending a hammer to understand how

credit and debt work in the network:

-

Alice lends Bob her hammer (Alice creates Alice-Hammer tokens)

-

Bob then lends the hammer to Carol (Bob creates Bob-Hammer tokens)

-

If Carol doesn't return the hammer to Bob, Bob still owes Alice a

hammer

-

This demonstrates how credit relationships are maintained

independently in the network

-

Each person is responsible for their own credit relationships,

regardless of what happens downstream